Data dive into the cost of living crisis

Section

Just as Europe is moving from emergency mode to recovery from devastating effects of COVID-19, the continent is now preparing for a new era of discontent brought on by a growing cost-of-living crisis. Inflationary pressure is becoming more persistent and broad-based. Funders are now turning their attention to how to collectively mitigate the impact being felt by communities as well as their employees, and grantee partners.

Philea provides this data dive into available research, and statistics alongside insights from philanthropic actors to inform our members about the scale and disparities of the problem as well as practical steps being taken by funders and their long-term considerations.

What is the cost of living crisis?

The cost of living crisis is a shorthand for describing the present situation where prices of products and services are rising significantly while nominal wages are not keeping up.

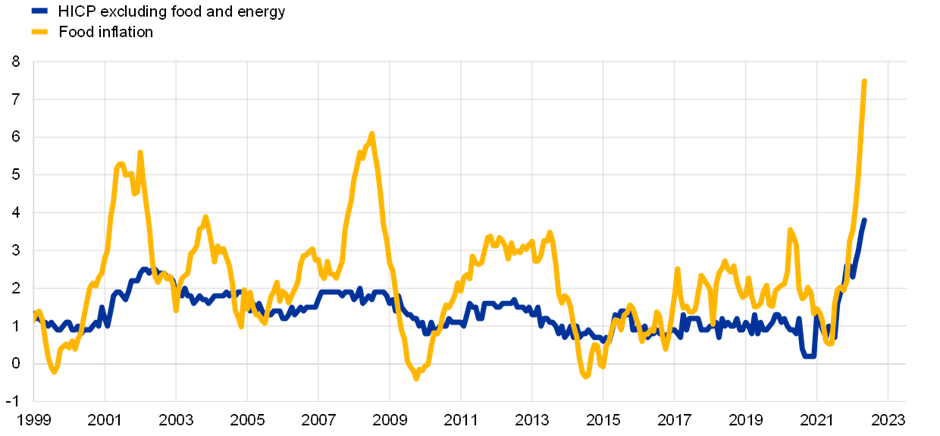

Source: Eurostat and ECB calculations

This portion of the briefing gives an overview of rising prices and the current state of the European economy which may provide important insights about the likely persistence of inflation, and what this may imply for the appropriate responses.

- Food price inflation in the European Union (EU) accelerated from the fourth quarter of 2021, reaching 3.5% in January 2022 and 7.5% in May 2022, the highest level since the beginning of monetary union.

- It is important to remember regional differences in Europe. The problem is particularly severe in Central and Eastern Europe (CEE), where wages are generally lower than in the West. In many CEE countries, the increase in the average price for food was around twice or more compared to overall EU rate, according to statistics agency Eurostat.

- Retail electricity prices for household costumers in EU capital cities were up by 44% in May 2022, compared to the same month in 2021. In August 2022, the price of bread in the EU was on average 18% higher than in August 2021.

- Rising energy costs has also an impact on the planet. The fossil fuel generation in the EU increased by 6% year-on-year in Q1 2022. Based on DG for Energy’s preliminary estimates, the Q1 2022 carbon footprint of the EU power sector rose by 8% compared to Q1 2021.

- Increasing consistently since mid-2021, EU annual inflation was 10.9% in September 2022, up from 10.1% in August (A year earlier, the rate was 3.6%). That is more than five times the 2% target set by the European Central Bank.

- The European Commission’s latest economic forecast (July 2022) also gave a negative view of what is coming. It is predicted that inflation will remain high throughout 2022 and 2023, dropping only to 4.6% in the EU next year.

- Europe’s advanced economies will grow by just 0.6 percent next year according to projections in latest World Economic Outlook (October 2022).

- The European Central Bank has raised interest rates for the first time in more than 11 years as it tries to control soaring eurozone inflation.

- As central banks across the world simultaneously hike interest rates in response to inflation, the world may be edging toward a global recession in 2023 and a string of financial crises in emerging market and developing economies that would do them lasting harm, according to a comprehensive new study by the World Bank.

Human impacts of the cost of living crisis

The rising energy and food prices are affecting lives in Europe and around the world. Here is how:

- 71 million people have fallen into poverty in just three months (March-June 2022) as a direct consequence of global food and energy price surges. The impact on poverty rates is drastically faster than the shock of the COVID-19 pandemic, according to the UN Development Programme (UNDP).

- Even in the most high-income countries, people are going without food. In May, an Ipsos poll for the World Economic Forum found that 1 in 4 people were struggling financially in 11 high income countries

- Open Society Foundation’s polling in 22 countries of more than 21,000 citizens found almost half of respondents (49 percent) listed cost of living and inflation concerns as one of the top three challenges facing their family and community today. In Western Europe, 33 percent agreed to some extent with the statement “I often worry about whether my family will go hungry’’.

- The report by IRI reveals that 58% of respondents surveyed in Europe’s some of the largest economies (France, Italy, Germany, Spain, UK and Netherlands) have now cut down on essentials (driving to work or shop, missing meals and reducing heating) with 35% dipping into their personal savings and taking out loans to pay bills.

- Rising interest rates increase the cost of mortgages for owner-occupiers, whilst landlords pass on rising costs to tenants, putting pressure on stretched family budgets.

- The rising cost of living has also been associated with a reduction in wellbeing, including increased anxiety and worsening mental health. Research by the British Association for Counselling and Psychotherapy found that 66% of therapists cite cost of living concerns as negatively impacting people’s mental health,

- YouGov European cost of living tracker monitoring attitudes on this issue across seven European countries (Britain, France, Germany, Spain, Italy, Sweden and Denmark) found that eight in ten (82%) say the government managing the issue badly, including 55% who say they are doing “very badly”.

- The crisis could threaten social cohesion in Europe and elsewhere. According to the study conducted by More in Common in the UK, Germany, France and Poland, people in all countries are worried about potential social upheaval, fearing protests, strikes and people going hungry over the winter. Anger is rising and spilling out on to the streets. The cost of living protests are already happening across France, Belgium, Germany, the Czech Republic and Spain.

The crisis impact people differently

Everyone is hurt by inflation, but disability status, ethnicity, gender, income level, and home ownership status disproportionately affect people’s ability to afford their basic needs.

- In Opinions and Lifestyle Survey (OPN) conducted in the UK, 69% of Black or Black British adults and 59% of Asian or Asian British adults reported difficulty affording energy bills, compared with 44% of White adults. 55% of disabled adults found it very or somewhat difficult to afford energy bills, compared with 40% of non-disabled adults. 36% of disabled adults reported difficulty affording rent or mortgage payments, compared with 27% of non-disabled adults. 60% of renters reported difficulty affording energy bills compared with 43% of those with a mortgage. 39% of renters reported difficulty affording their rent, whereas 23% of those with a mortgage reported difficulty affording their mortgage.

- European Disability Forum flags that persons with disabilities, which already experience higher poverty rates, have to face extra costs related to living in an inaccessible world. Prices are higher while disability allowances and salaries diminish or stay the same. Assistive technologies have become more expensive, pushing persons with disabilities deeper into poverty. Elevated energy costs limit the use of heating, aggravating chronic pain and health issues.

- The cost-of-living crisis is expected to hit women the hardest with a widening gender gap in the labour force, warned the annual Gender Gap Report 2022 of the World Economic Forum. The spikes in inflation have a more significant impact on women compared to men due to their prevalence in low paid roles, lower wages and spending commitments (such as non-durable household goods and childcare).

- The study conducted by the Living Wage Foundation, found that during a period of unprecedented rises to the cost-of-living 42 percent of low paid women had fallen behind on household bills, compared to 35 percent of low paid men and that 35 percent of low paid women had skipped meals regularly for financial reasons, compared to 29 percent of low paid men. Moreover, 50 percent of low paid women said their levels of pay negatively affected their levels of anxiety, compared to 38 percent of low paid men; and that 48 percent of low paid women said their levels of pay negatively impacted their overall quality of life, compared to 36 percent of low paid men. The report explains that it is due to gendered expectations such as disproportionate responsibility for household shopping, meaning many women notice variations in prices and feel the stresses of inflation more acutely.

- UNWomen stresses that these difficulties are particularly challenging for rural women, who face additional hurdles such as poor access to resources, services and information, the heavy burden of unpaid care and domestic work, and discriminatory traditional social norms.

- According to FEANTSA, the European Federation of National Organisations Working with the Homeless, low-income households will be worst hit by rising costs and a likely recession. They already spend a high proportion of their income on essentials like food, heating and housing. They are not able to cut back without undermining their well-being because they are already using the minimum, or less. They also have less choice and control about what and how they consume.

- Leader Unlocked’s youth-led research about the effects of the cost of living crisis on young adults across the UK found that young adults’ physical and mental health has been severely impacted by the cost of living crisis. More severe effects are being felt by minoritised ethnic groups, women, trans people, people with non-binary gender identities, and people in receipt of benefits.

Diverging views on drivers of the crisis and measures to deal with it

The cost of living crisis has recently dominated debate among politicians, the public, the economists, journalists, trade unions, the civil society and other societal actors. The current cost-of-living crisis is being commonly attributed to two macro-economic shocks: Covid-19 and the war in Ukraine. Russia, supplier of about 40 percent of EU gas consumption, has reduced its deliveries to the EU by 75 percent (up to September 2022). Moreover, the war in Ukraine, as well as sanctions against Russia, have resulted in a massive decline in the supply of major staple foods, leading to a rise in food prices globally. Even if there is a broad-base agreement of the drivers of the crisis, there are diverging opinions when it comes to identify what measures should be taken. Is the cost of living crisis best met with caution and help for the neediest, or by slashing taxes and “going for growth”? Although it is a non-exhaustive overview, the following sections provides a snapshot of different views on what needs to be done on short and long term.

- A mainstream economist view: According to Vicky Pryce, Chief Economic Adviser at the Centre for Economics and Business Research, the problem now is that demand-pull inflation, which we experienced when Covid restrictions were lifted and the economy surged, has turned into cost-push inflation (this type of inflation is caused by increases in the cost of important goods or services where no suitable alternative is available), determined not by wage growth but by the war in Ukraine, which has sent energy and food prices soaring. No central bank by itself can do much about this, except through lowering growth and possibly bringing about a recession – or even depression.

- An alternative economist view: Some economists argue that the crisis has been exacerbated by short-term factors, such as the Ukraine war, but the pressure on living standards has long-term trends as the prevailing economic system has been failing most people and the planet. Therefore, the solution would not come from focusing on the symptoms of the crisis. ‘’It’s time to rethink the institutional arrangements dominating modern economic policy… to control inflation and drive the transition to a fair, sustainable economy’’ says David Barmes, Senior Economist at Positive Money.

- Financial institution’s prescriptions: Financial institutions, such as IMF, recommend governments to maintain a tight fiscal stance to help fight inflation so that fiscal policy does not work at cross-purposes with monetary policy. ‘’Targeted fiscal support can help cushion the impact [of rising prices] on the most vulnerable, but with government budgets stretched by the pandemic and the need for a disinflationary overall macroeconomic policy stance, such policies will need to be offset by increased taxes or lower government spending’’ the World Economic Outlook (July 2022) states.

- UNDP’s warnings: Governments are bringing in measures designed to ease the impact of inflation, including tax cuts, free train travel, energy subsidies and cash transfers. However, the UNDP report warns that not all policies will be equally effective and some may disproportionately benefit wealthier people.

- Labour unions’ demands: Labour unions call on politicians and employers to avoid the same mistakes of austerity policies deployed during the 2008 crisis, reminding that wage restraint, coupled with massive cuts to public expenditure will only lead to a longer period of depression and possible social unrest. IndustrialAll Europe has recently launched a campaign with five key messages: (1) a pay rise that guarantees decent living standards, (2) fair taxes on companies and the wealthy, (3) support for workers affected by the cost-of-living crisis, (4) financial support for companies struggling with energy costs, with guarantees to save jobs and raise wages, (5) sectoral bargaining so workers can win better pay

- Charity asks from national governments: Similar to trade unions in Europe, a coalition of 40-plus charities and grassroots groups from the UK lately launched a campaign called Stop the Squeeze pushing for politicians to adopt tougher policies on wealth taxation, amid fears of spending cuts to plug public finances.

- Low trust citizens’ expectations: Citizens survey conducted by More in Common demonstrate that many – particularly among low trust groups – need immediate relief before they can look ahead. Policies that garner the most support combine short term solutions (tax cuts, price caps, taxing windfall profits and providing free alternatives to driving) as well as clear plans for long term investments.

- Expert view on framing: Some commentators argue the term cost of living crisis is poor for many reasons, foremost, crisis framing obscure what is driving the situation, fuelling fatalism (things can’t and won’t change), fostering helplessness, and narrowing people’s thinking on short-term, immediate relief rather than the long-term or systemic solutions.

Official responses to the cost of living crisis

- Government responses: European countries have been taking various action to tackle the cost of living crisis. Countries such as the Netherlands, Poland, Germany, Spain, Italy, Belgium and France have reduced taxes on electricity, petrol, and heating. These countries also offered one-off payments and subsidies to low-income households to support them in paying energy bill Spain has introduced free train travel on all regional and medium-distance train.. Additional measures, such as tax credits for industries with high energy usage were introduced in Italy. Ireland commits €11 billion to fight cost-of-living crisis without going into deficit thanks to its ever-rising collection of tax from the profits of 1,700 foreign multinationals based in the country.

- The EU’s response: The EU is introducing: (1) “solidarity levy” – a windfall tax – on excess profits made by oil, gas, coal and refinery companies in 2022; (2) A cap on the revenues of electricity companies which produce energy from wind, solar and nuclear. These revenues have risen as the price of electricity from these sources is linked to soaring gas prices – the cap is expected to raise €140 billion; (3) A mandatory reduction of electricity consumption in peak hours by 5% across the EU, until March 2023; (4) A voluntary reduction of 10% of overall electricity consumption – individual countries will decide how to this.

How are charities affected by the crisis

Charities are impacted by the cost of living crisis in numerous ways:

- Charities face the same inflationary pressures as households. As the prices are rising, running costs of charities are increasing as well. Unlike businesses, they can’t simply raise prices or switch out unprofitable product lines. Depending on their areas of activity and size, some charities will experience the sharpest price increase, especially small, local, community-based organisations providing human services and consumer goods to those in need.

- An operating reserve is an undesignated portion of a charity’s net assets that is set aside to sustain the organisation through unexpected challenges. Inflation will lead to loss in value of these reserves more quickly than what was previously forecasted. Charities may need to review how their reserves are managed and make necessary change urgently to maintain their value against inflation.

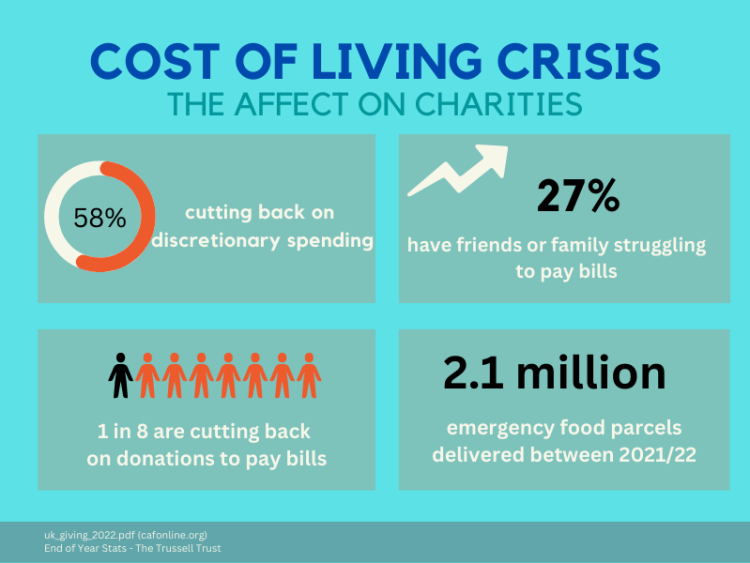

- Charities will see the value of grant income and donations decline. Pro Bono Economics calculated that on current forecasts of inflation in UK (March 2022), a £100,000 grant will be worth £88,100 by 2024

- As the cost-of-living crisis drive up demand on service, coming hot on the heels of the Covid-19 pandemic, charity staff providing frontline services are under immense stress. Research conducted by Third Sector found that 94.3% of charity workers had felt stressed, overwhelmed or burnt out over the past year. In addition physical, emotional, and mental exhaustion brought by the crisis, low wages make it difficult to justify staying in the sector.

- Charitable giving usually declines during economic downturns when it is needed more than usual. Nearly nine in 10 (86%) charity leaders anticipate that demand for their services is likely to increase. That means charities will be expected to do more with fewer financial resources as there is a fall in household donations. The CAF UK Giving Report 2022 found that fewer people are giving to charity overall, a trend exacerbated by rising living costs. Many people say they plan to rein in their budgets further with rising costs for their own energy and fuel bills, including one in eight (13%) cutting back on charity donations.

Source: Charities Aid Foundation

Funders’ responses to mitigate the impact of the crisis on charities

Funders which paid out more than usual through the pandemic have hoped to return previous levels of giving and move their focus back to strategic initiatives, rather than operating in emergency mode. Philanthropic leaders are asking whether it is their call again to step in to fill the financing gaps or whether it is governments’ duty to increase benefits amid cost of living crisis.

Philanthropies can bring innovation to welfare policies but cannot be inexpensive policy alternative to ensuring an adequate standard of living for welfare-reliant households. Foundation leaders are weighing where they can make more difference with their limited funds at these critical times shaped by multiple crises.

At a time like this many organisations and individuals look to the foundations. We asked foundations whether they agree that foundations’ reputation individually and collectively will be shaped by their response at this time, and we received different responses.

- Those who strongly agree with this statement believe that with the devaluation of grants, standing still will be a real time cut; hence flexible funding and responsive model emerged during the pandemic should become the norm here.

- Those who somewhat agree argue that funded partners (and the sector in general) know funders are not magicians unless they have very deep pockets. Foundations can aim to be equitable and pragmatic rather than coming up with a solution that fits everyone.

- Those who neither agree nor disagree say that we should not overestimate the role of philanthropy in solving macro level problems.

- Those who somewhat disagree claim that foundation should be strategic and use other tools to make grantees more resilient (such as organisational development support) because the crises are manifold. This is society-level, black swan change, which requires a larger question about we foundations do and how to tackle the root causes of this instability in the mid / long term.

Many foundations have already been responding to the reality of ongoing inflation while others haven’t yet made decisions, and are eager to hear how peer organisations are responding. Therefore, we hope the practices and considerations shared here may inspire your actions.

- Tying giving to the most recent measure of inflation: Some foundations add an extra percentage to their grant amount in line with the rate of inflation in countries they focus. They would like to make sure that their grantees do not have to choose between supporting staff and investing in their program growth due to heightened budget constraints.

Increasing grants by a certain percentage requires the consideration whether it will be one-time bump or a new baseline for the next instalment of multi-year grants and renewal. This means exceeding original grants budget for the current and following years, which may not be easy especially for foundations with narrowly written perpetuity clauses.

In the last two years, returns on endowments having done well despite Covid-19. Foundation leaders are now assessing to what extent they are ready to redirect that increased income towards additional support to deal with the cost of living crisis if endowment performance remains stable or evolves beneficially.

- Adopting a case-by-case approach: The foundations that are hesitant to take a one-size-fits-all approach consider factors like the longevity of their funding, recent changes in the grant size, grantees’ particular budget changes for the year, and the size of grantees’ financial reserves.

In order to tailor their support to grantees’ actual needs, foundations talk to grantees to understand how costs and demands are changing. By doing so, they are also able to assess where the impact of not uplifting will cause the most harm.

While studying their existing grants and their real value, foundations also monitor the national policies (such as caps on energy prices, and relief packages directed to households and charities) and adapt their interventions accordingly.

- Launching specific hardship funds: As an alternative to increasing existing grants, foundations provide small grants to charities and community groups. These funds enable grantees to meet additional costs, either to be distributed to service users or support operational spending.

- Supporting financial health: Financial resilience in charities means having strong financial foundation, cash reserves, an expansive and diversified revenue stream, and financial flexibility to be prepared to sustain themselves and their missions no matter the challenges ahead. Investing in long-term financial stability through multi-year, core grants as well as non-financial organisational development support is one of the strongest ways for going beyond short-term remedies and increasing charities’ readiness for what’s next.

- Applying lessons learnt from the pandemic experience: When Covid-19 took hold, funders responded swiftly, launching emergency grants, providing flexible and unrestricted support, easing application and reporting procedures, and focusing on overall capacity and resilience of grantees. Some charities are concerned that with the lift of COVID restrictions, funders have reverted to old, project-base models of funding.

There are calls within and to philanthropic community to take a strategic step back to take stock of what we have learnt from pandemic experience and, build on the best practices to create a real paradigm shift. Unrestricted grants are particularly precious at this moment as they enable charities to become agile to deliver the most effective means of supporting the people they serve.

So far, the most popular responses within the Philea membership include the following actions:

- Increasing giving to take account of rising costs a

- Improving the grant-making processes with more clarity about what the organisation is doing (or cannot do) so that grantees can optimize their time, energy and resources

- Considering collaboration as a way to make funding go further

- Talking with grantees to understand how inflation, increased prices, and rising needs are impacting them and how to help

- Switching to unrestricted funding or full cost recovery grants to help grantees better manage the impacts of inflation

- Increasing multi-year grants in line with inflation

Less popular actions:

- Thinking in the long term and look at how grants and investments have developed over the past decade, not just the past 12 months

- Considering the impacts of what the rise in the cost of living means for different organisations working with different target groups or providing specific services

- Supporting grantee organisations to be good employers – don’t inadvertently push down wages or conditions

Funders’ responses to mitigate the impact of the crisis on employees

In addition to their responsibility to support their grantees, philanthropic organisations need to take care of their employees and support their financial and mental wellbeing as good employers. Foundations take measures targeting foremost staff members who are under a certain earning threshold and at the risk of financial insecurity. As one can imagine naturally following actions are not coming at the expense of grant increases.

- Pay rise: Foundations implement salary increases especially for lower-paid staff, at different ranges (something between 2-10 percent). Different references are used to determine the percentage of indexation, including The Retail Price Index, The Consumer Price Index, and the agreements of the trade union for the concerning sector etc. In some counties where automatic indexation is required by law, pay rise is not at the discretion of the employer. Where governments even out the energy costs for households, foundations tend to apply an indexation percentage that reflects the current inflation rate excluding energy costs.

- ‘One-off’ bonuses: One-time payments which help employees in the short run to deal with immediate financial difficulties are less popular than indexation. While a few foundations offer this to all staff members, it is more common to give this bonus to staff in lower pay bands who will be most impacted by the higher costs of basic goods.

- Other financial support alternatives: Foundations which are considering the previous options attempt to support their employees with their costs by providing free lunches, vouchers or subsidies for lunch, travel, cycling equipment, sports.

- Financial guidance: Foundations are aware that providing financial guidance alone will not solve financial hardship and should be considered only if it is accompanied with financial support, otherwise it may have a backlash.

- Mental health support: Mental health and financial concerns are often intricately linked. All employers are now urged to help staff members navigate stresses of the cost of living crisis. Even small things may make a big difference to create the right culture, from providing a quite room in the office to organising check-ins on staff.

Contact